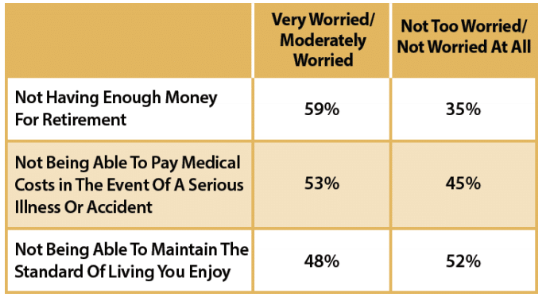

According to the Center for Retirement Research at Boston College, 53% of American households are at risk of not having saved enough to maintain their current living standards and retirement in fact, a recent Gallup Poll shows Americans’ #1 fear is running out of money in retirement. Traditional sources of retirement are becoming less effective. The social security is running out of money, anew ruling in California paves the way for pensions to betrimmed or eliminated by bankruptcy, and stock market volatility makes depending on 401(k)s riskier than ever before. More and more American workers are delaying retirement because they lost significantly in the 2008 crash. Instead of focusing on saving up for a million-dollar nest egg, the savvy American knows that incoming cash flow are the key to security.

Financial advisors traditionally recommend that you withdraw no more than 4% of your nest egg each year to ensure that you will have enough money to last your lifetime. This advice might actually be putting a retirement at risk. Let’s look at how well that’s going to turn out for the rare person who actually has saved a million dollars.

4% of 1 million is $40,000 per year, but remember this is before taxes. At a 21% tax rate (15% federal and 6% state), your income is down to $31,600 per year, or just over $2,600 per month. And this assumes tax rates never go up. And that’s assuming no losses.

What happens if your account has one single 30% crash during your retirement? Your $1,000,000 is now $700,000 and at 4%, that means $28,000 before tax, and $22,120 after tax or just $1,843 per month.

Does that sound like the retirement of your dreams?

This advice may have been sound in the early 1900s, but too much has changed to rely on this old, outdated advice in the volatile world we now live in. Things like longer lifespan, increasing taxes, market crashes and massive increases in health care expenses make questionable to rely on the 4% rule for your retirement

You don’t have to give up living a full and rewarding life just to make sure you don’t run out of money in retirement. The conventional wisdom says you must stop spending, and hope your nest egg lasts longer than you do. What kind of retirement does that sound like? Do you want to spend your retirement on the couch watching reruns? Or would you rather travel the world, visit your kids and grandkids, and enjoy the hobbies you’ve always wanted to spend time on?

The IUL is an innovative cash value insurance policy that potentially solves the number one problem people fear: running out of money and retirement. It can create a supplemental tax-advantaged cash flow that could potentially last for the rest of your life by combining the unique participating loan feature where your cash value can grow while you access your money and give you the death benefit you need.

Your cash value can potentially grow double digits and is still protected against market crashes. The IUL Insurance policy also provides death benefit.

Let’s take for example a 41-year-old who wants to retire at 65.

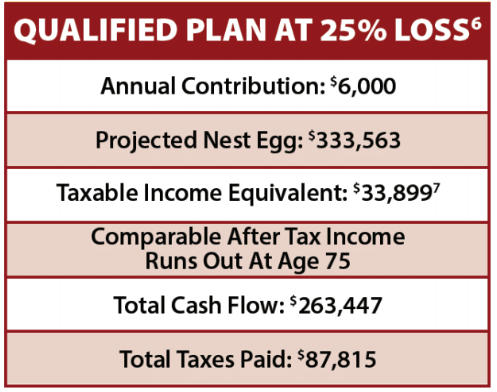

IRA: This projection assumes 7% growth. The full $6,000 is deposited because taxes are deferred until withdrawal. Total taxes paid are $87,816. In order to get $25,424 spendable income the subject would need to withdraw $33,899 because taxes have to be paid on this money. At this rate the subject will run out of money at 85. The IRA provides $263,447 in total cash flow after taxes.

Other Important Facts About Qualified Plans:

• Fully taxable in retirement

• Money at risk to losses

• Gains subject to market volatility

• Limited access to funds

• Exposure to higher taxes rates in the future

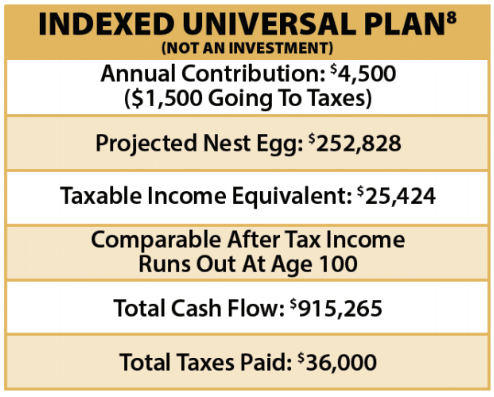

IUL: This projection also assumes 7% growth. Taxes are paid upfront, so only $4,500 goes into the policy. The total taxes paid are $36,000. The tax-free cash flow of $25,424 could continue to age 100.

The IUL provides $915,265 in total cash flow lasting to age 100.

Other important facts about the IUL:

• Tax-advantaged in retirement

• No risk of loss in stock market

• Gains are locked in each year

• Tax-free cash flow could last to age 100

• Potential for double digit growth

Remember: The IUL is a tax-advantaged life insurance policy which means you pay taxes upfront and never pay taxes on that money again (unless contract is surrendered).

If you are thinking about and planning for retirement, then you are already taking a step in the right direction. However, there are many factors to consider and this quiz will provide a current and realistic summary of where you are versus where you want to be in terms of retirement readiness.

We highly recommend Andy and Sheri to review your options for insurance and wealth building. They are very open, respectful, and accommodating, with great options for any stage of life.

Katrina & Steve S.

We highly recommend Andy and Sheri to review your options for insurance and wealth building. They are very open, respectful, and accommodating, with great options for any stage of life.

Katrina & Steve S.

We highly recommend Andy and Sheri to review your options for insurance and wealth building. They are very open, respectful, and accommodating, with great options for any stage of life.

Katrina & Steve S.

We highly recommend Andy and Sheri to review your options for insurance and wealth building. They are very open, respectful, and accommodating, with great options for any stage of life.

Katrina & Steve S.

Regardless of your stage in life and your needs, we can help you. Please feel free to schedule an appointment or reach out to us directly.