Wall Street loves to promote compound interest as the eighth wonder of the world because it’s a sales tactic for convincing people to invest in mutual funds and the stock market. Compound interest is great in theory, but in reality, it doesn’t exist in the stock market.

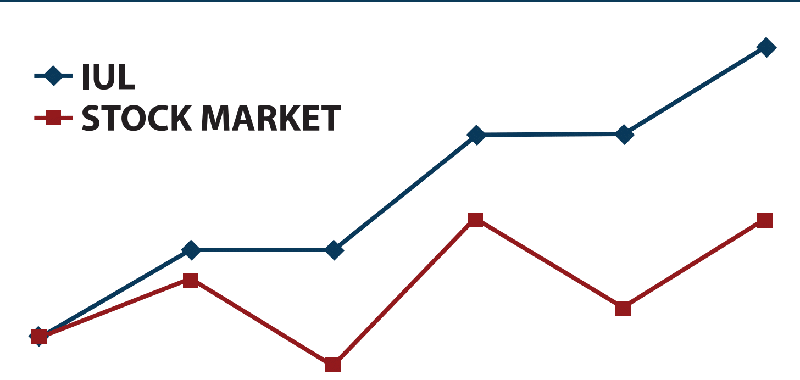

Here is why; Compound interest only works when you don’t lose the principal. The graph below shows the growth with an Indexed Life Insurance Policy versus the typical ups and downs of the stock market.

IUL: every year the market goes up, your cash value grows. There is no wasted time making up for losses. The IUL performs well in times of volatility because it captures the upswings after the downturns. The IUL is an Indexed Universal Life Insurance Policy.

Stock Market: this is not compound interest. Because many of the gains are making up for past losses.

During this time the market rose 25% sounds good, right?

Over 14 years has only a 1.78% increase per year. And once you adjust for inflation the return actually goes to a negative .67%.

Why so low? You guessed it. The Enemy Of Wealth: MARKET LOSS.

There is a solution. We call it an IUL. An IUL is a uniquely structured cash value insurance policy that can provide potential for double-digit growth during good years and complete downside production from stock market crashes. And, unlike the stock market rollercoaster, you enjoy constant growth with an IUL because when the stock market drops, your principal doesn’t decrease. It stays level, and because of that, when the market rebounds you immediately start to experience growth on your money again… Picking up where you left off. This is the key to growing your wealth. You never lose money or time making up for losses.

Just one of the flaws is the claim from people like Dave Ramsey that the average American can actually get a 12% to 15% return investing in mutual funds and stocks (Source:www.daveramsey.com). But let’s look at the reality. On January 1st 2000 the S&P 500 was at 1498.58. 14 years later on January 1st 2014 the S&P 500 closed at 1872.34 which is a 25% gain. Remember this is over 14 year period which equates to 1.78% per year…Before adjusting for inflation. And to make matters worse 84% of actively managed (mutual) funds underperformed the S&P 500’s 1.78% average. In addition, these returns leave out the effects of taxes and fees, which significantly reduce your wealth and retirement income. If this is the case, how do they come up with these high average rates of return?

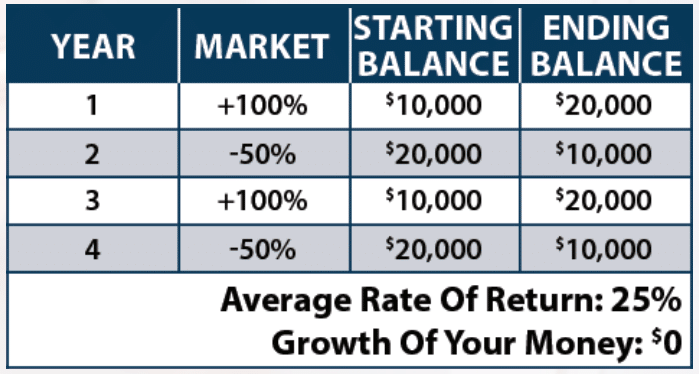

It’s Rate of Return Fuzzy Math. You’ll be amazed when you see how a 25% average rate of return could really net you absolutely nothing in your account. For example let’s say you start with $10,000 and in the first year you get a 100% rate of return, increasing your balance to $20,000. The next year the market drops by 50% leaving you with $10,000 again.

In year three, it goes up again by100% to $20,000. Then drops again by 50% down to $10,000

In this example, the market did average a 25% rate of return. But how much additional cash do you have left to show for your 25% rate of return? ZERO.

AND THAT’S THE RATE OF RETURN FUZZY MATH!

If you are thinking about and planning for retirement, then you are already taking a step in the right direction. However, there are many factors to consider and this quiz will provide a current and realistic summary of where you are versus where you want to be in terms of retirement readiness.

We highly recommend Andy and Sheri to review your options for insurance and wealth building. They are very open, respectful, and accommodating, with great options for any stage of life.

Katrina & Steve S.

We highly recommend Andy and Sheri to review your options for insurance and wealth building. They are very open, respectful, and accommodating, with great options for any stage of life.

Katrina & Steve S.

We highly recommend Andy and Sheri to review your options for insurance and wealth building. They are very open, respectful, and accommodating, with great options for any stage of life.

Katrina & Steve S.

We highly recommend Andy and Sheri to review your options for insurance and wealth building. They are very open, respectful, and accommodating, with great options for any stage of life.

Katrina & Steve S.

Regardless of your stage in life and your needs, we can help you. Please feel free to schedule an appointment or reach out to us directly.