David M. Walker may be the most knowledgeable man alive when it comes to our country’s fiscal state. He served as the Comptroller General of the United States and as the head of the Government Accountability Office for 11 years under two presidents. This is the guy who knows a thing or two about the country’s finances.

He appeared on national radio and delivered the grim news that based on the current fiscal pattern, future tax rates would have to double or the country could go bankrupt. His reasoning? Simple math. The debts and obligations of the country must be paid. The United States currently spends roughly 76 cents on every dollar it brings in on four items: social security, Medicare, Medicaid, and interest on national debt. Continuing on the same course we are on now, that could grow to 92 cents of every dollar by the year 2020.

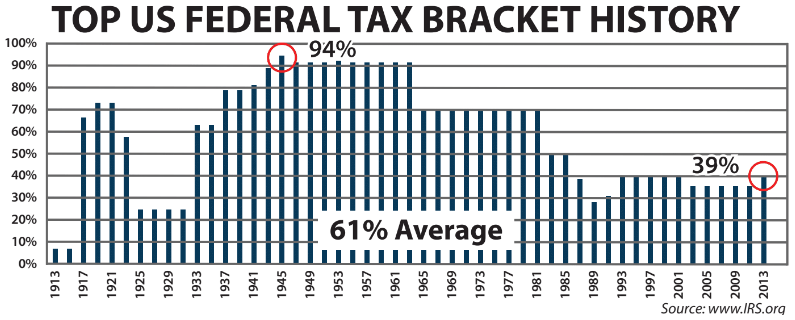

According to Walker, social security was never intended to be a retirement program. It was merely insurance against living too long. In fact they set the retirement age at 65 years old, knowing life expectancy was just 62 years old… They were counting on most people dying before they ever used it. Luckily there is a solution; the indexed life policy. Does doubling tax rates sound crazy? Well it’s not. Just take a look at the history of tax rates in this country. You can see at one point the top tax rate was 94%. 94%! And this is just at the federal level, not including state taxes.

During the fiscal year of 2014, Washington took in a record revenue of $2.4 trillion dollars but still managed to spend $500 billion more. This shows their unquenchable appetite for spending. So, how can you be sure the tax rates won’t significantly increase over your lifetime? You can’t. This is exactly why it can be dangerous to defer all your taxes until retirement using tax-deferred qualified plans.

Many people think that could never happen in the good old USA. WRONG. It might surprise you to know that President Franklin D. Roosevelt actually passed an executive order in 1942 effectively taxing 100% of income over$25,000.100% taxation, complete confiscation of all income over $25,000. Fortunately, Congress fought it back to just a 94% top tax bracket.

“In order to correct gross inequalities and to provide a greater equality in contributing to the war effort, the Director is authorized to take the approperiate regulations, so that, insofar as practicable no salary shall be authorized under Title III, Section 4, to the extent that is exceeds $25,000 after the payment of taxes allocable to the sum in excess of $25,000.”

So, how do you protect yourself against higher tax rates? If you listen to the gurus on TV and Wall Street “experts” you’ll hear a lot about maxing out your 401(k) and IRA contributions in order to get a tax deduction and grow your money tax-deferred.

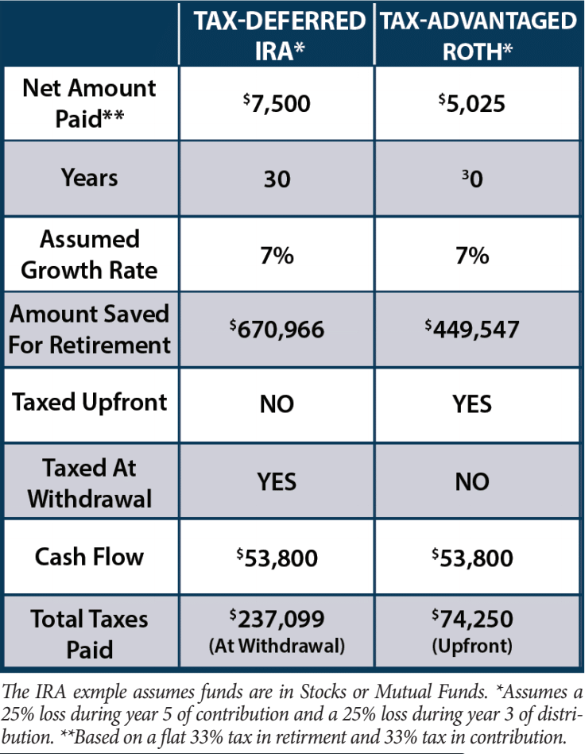

Knowing taxes are likely to be higher in the future, why would you trade in a lower tax rate today for a future rate that could be much higher when you need the money most? Don’t take my word for it, just look at the math. Here we’ll compare paying taxes today and creating tax-free retirement cash to deferring taxes to the future: In this example, let’s say you contribute about $7,500 per year for 30 years.

With an IRA you paid no taxes on that money because you got a deduction, on the other side you would have paid tax at your normal income tax rate, let’s assume 33% for state and federal taxes. With the tax-advantaged approach, you would pay $74,250 in taxes ($2,475 per year x 30 years). In this example, when you retire (assuming just one loss of 25% in year five of contribution) you’ll have $670,966 in the tax-deferred plan or $449,547 in the tax-advantaged plan. You’re probably thinking this is a no-brainer — I’ll take the tax-deferred plan with the bigger balance. But there is a catch. Let’s say you take out $53,800 a year to live on during retirement. Assuming your money is still growing at 7%, you can take $53,800 a year for 9 years. However, each year you will have to pay $26,498 in taxes on that money. That means you could end up paying $237,099 in taxes versus $74,250 with the tax-advantaged plan.

And this assumes taxes never go up. Now that you know the truth; how do you feel about paying three to five times more taxes than you would with a tax-advantaged plan?

Think of it like this: when you invest any 401(k) or an IRA, the IRS will get paid. Right now they agreed to take about a 30% share (the current tax rates). What if they decide instead of 30% that they want to take 40% or 50%? What control do you have? Would you enter a business partnership where your partner can change the rules at any time? Of course not. The reality is, it’s hard for to plan for retirement if you don’t know what share of your money is really yours.

If you are thinking about and planning for retirement, then you are already taking a step in the right direction. However, there are many factors to consider and this quiz will provide a current and realistic summary of where you are versus where you want to be in terms of retirement readiness.

We highly recommend Andy and Sheri to review your options for insurance and wealth building. They are very open, respectful, and accommodating, with great options for any stage of life.

Katrina & Steve S.

We highly recommend Andy and Sheri to review your options for insurance and wealth building. They are very open, respectful, and accommodating, with great options for any stage of life.

Katrina & Steve S.

We highly recommend Andy and Sheri to review your options for insurance and wealth building. They are very open, respectful, and accommodating, with great options for any stage of life.

Katrina & Steve S.

We highly recommend Andy and Sheri to review your options for insurance and wealth building. They are very open, respectful, and accommodating, with great options for any stage of life.

Katrina & Steve S.

Regardless of your stage in life and your needs, we can help you. Please feel free to schedule an appointment or reach out to us directly.